#028 Building an Antifragile Portfolio

Tue, 07 Feb 2023 09:00:29 GMT

Cornerstone Ventures

While 2021 was the year of Unicorns with 44 technology companies in India alone achieving the unicorn valuation, 2022 was a stark contrast. 2022 witnessed a major slowdown in global economic growth for various reasons (as detailed in our previous edition) leading to the biggest lay-offs and rationalization, especially in technology companies, since the global financial crisis of 2008.

Many global funds that were extremely active in deploying fresh capital throughout 2021, have either slowed-down on new investments in 2022 or have been focusing on getting their house in order after due to ripple effects of careless investments

While the other venture funds were chasing ‘growth-at-any-cost’, we kept our head down and continued to tread on the first principles of value-investing and value-chain control. We consciously slowed down fresh deployments in 2021 due to extremely high valuations. We knew this was unsustainable and had to come crashing down as the liquidity from the market would vanish. The start of 2022 proved us right! The markets came crashing down on the back of liquidity pull-back by the Fed and the valuations corrected across the board – especially for the technology sector and particularly for SaaS businesses that saw the maximum inflow of capital.

Technology was the worst impacted sector in 2022, where we saw companies lose significant valuation in the market correction. Even within technology sector, SaaS businesses were hit the worst due to excessive inflow of capital at very low cost, that suddenly dried-up.

We saw this as a unique opportunity to invest in great businesses available at reasonable valuations. We continue to believe that Technology is an inherently Antifragile sector and within this sector, Enterprise SaaS business have an added advantage.

Antifragility

Antifragile, a term coined by Nassim Nicholas Taleb, refers to systems that are positively impacted in the by short term volatility, adversity, or shocks. Antifragility is the true antithesis of fragility. It is beyond resilience or robustness.

The Fragile breaks; the Resilient endures; the Antifragile strengthens !

A classic example of antifragility is the human immune system. Every time a human is infected, the immune system develops antibodies to fight the infection and the ability to avert similar infections in future. Thus, with every infection, the human immune system becomes stronger and better than ever. More so, the newly acquired immunities are passed on to the next generation so that they don’t have to build it from scratch – a scalable antifragile system!

Technology - an Antifragile sector

Every economic crisis pushes enterprises to focus on cost-efficiencies and improving margins – providing a strong tailwind to new-age technologies that can enable operations at lower cost. As the economic situation start improving and enterprises start growing at healthy rates, they require solutions that can help them sustain the growth momentum at fractional cost, leading to adoption of revenue enhancing solutions.

Hence, every economic shock leads to the emergence and accelerated adoption of two breeds of technologies – (1) cost optimization solutions and (2) revenue enhancement solutions.

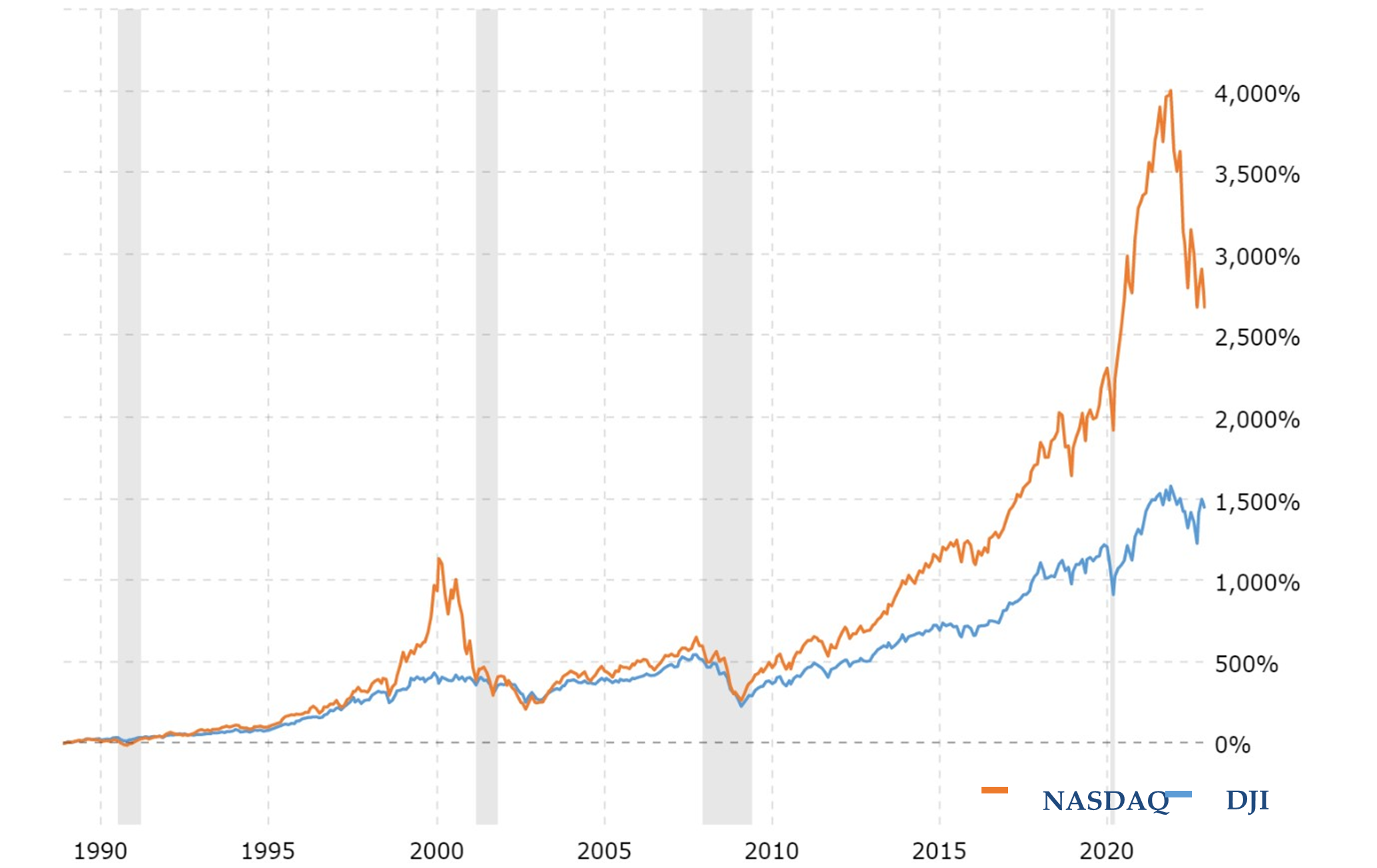

Below is a chart of Nasdaq Composite’s performance over the past 30 years, where the world has seen 4 major economic setbacks (the respective periods highlighted in grey).

Nasdaq grew by ~1000% post the crisis of 1990s; ~200% post the dot-com bubble of 2000s; and ~800% post the 2008 financial crisis up till the post-pandemic slowdown of 2021

Comparing this to Dow Jones’ performance over the same period - it grew by just ~350% post the crisis of 1990s; ~33% post the dot-com bubble; and ~300% post the 2008 financial crisis.

It’s evident that every single economic shock has setup the Technology sector for outperformance with new breed of companies leading the growth.

The dot-com bubble of 2000, led to the emergence of large tech platforms like Google and Facebook that capitalized on the growing penetration of internet and provided enterprises an entirely new paradigm of digital advertising and marketing.

The global crisis of 2008 led to the accelerated adoption of cloud technology due to its cost effectiveness, creating market leaders like AWS, Nvidia and Salesforce in their respective domains.

Enterprise SaaS emerged a winning pricing model for many cloud companies post 2010, but the struggle of adoption and pricing continued.

The Covid-19 pandemic boosted the adoption of Enterprise SaaS solutions across segments and companies like Snowflake, Zoom, etc. saw an unprecedented demand during the pandemic and global lockdowns. The enterprises realized the need of such solution for scalability and continuity – making enterprise SaaS solutions an absolute necessity for sales and business operations.

We believe the current economic slowdown is helping the Enterprise SaaS companies deliver “value” to their customers – in turn making a strong case for better pricing and value-capture. Over the next few quarters, we will see the emergence of innovative SaaS pricing that will enable the Enterprise SaaS companies to capture a larger pie of the value-chain. Example: Subscription pricing like Amazon Prime has scaled up from pure-play fixed subscription to a fixed minimum subscription + pay per use pricing to capture higher value from high-usage customers.

Similarly, many such innovative pricing models are emerging as the customers have realized the value of these products over the past few years and are willing to pay more. The companies with stronger pricing models will continue growing profitably – forcing the fragile businesses to scale-down and leaving the market to be captured by the antifragile !

The Indian Economic Outlook

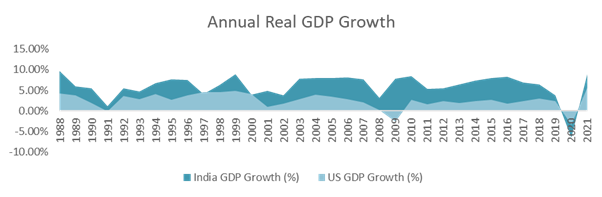

Historically, after every global slowdown, Indian economy has managed to bounce back stronger and higher than the global economy in just one year. This is primarily due to the timely structural reforms undertaken, coupled with favorable demographics and inherent ability to adapt to changing trends.

For eg: India abolished its licensing policy in 1991 and opened the economy for globalization and privatization – creating mammoth industries in just few years. The Indian IT companies capitalized on the dot-com crisis to realign themselves as the most cost-efficient outsourcing destination for IT services. In 2016, the introduction of GST unified the taxation system across the country, leading to structural shift to organized sector and uniform taxation across all industries.

The ‘Make in India’ initiative helped Indian companies to significantly reduce its dependence on the global vendors – a strategic decoupling from the world that proves to be a great advantage for the Indian economy in the current global situation. As per the economists, India will be the fastest growing economy in 202324 on the back of prudent financial management by the RBI, strong domestic demand & supply and inclusive initiatives by the government.

We expect accelerated adoption of digital solutions – even faster than in the pandemic, primarily driven by the need of enterprises to grow consistently and profitably. This underlying current will keep the economic growth engine running, ensuring that India continues to grow its economy in higher single digits for the next 2 years and reach a double digit growth by 2025.

Transcending to Antifragile SaaS

Throughout 2020 and 2021, we were focused on investing in resilient SaaS businesses – businesses that could withstand pandemic and economic downturns without any distress.

At the start of 2022, we realized that investing in resilient business wasn’t enough. The uncertainty and volatility in the markets is here to stay for long, perhaps throughout 2023. We expect 2023 to be a year of extreme volatility as the world recovers from the shocks of 2022 and readjusts to the new normal. Hence, we decided to invest in businesses that could not only survive the volatility, but rather thrive and grow stronger than its competitors.

Antifragile portfolios are built to outperform in a growing economy and minimize the capital risk in case of economic downturns. Antifragile portfolio are built to maximize the return while minimizing the risk. The individual investments or asset classes in the portfolio itself are antifragile in nature - with every shock or volatility in the economy, the weaker investments are weeded out and the exposure to the outperforming investments or assets is increased – thus improving the overall performance of the portfolio over time.

We have intrinsically adopted the concept of antifragility in our investment thesis and portfolio allocation strategies. Our top-down investment thesis has been a conscious selection of an antifragile business model, from an antifragile sector in an antifragile economy – Enterprise SaaS from the Technology sector in India ! This inherently makes our investment approach an antifragile approach.

Our every investment is carefully chosen to build a diversified concentrated portfolio – large bets spread across a few un-correlated sectors. This helps maximizing the returns while minimizing the risk. A few early bets in emerging technologies also help to improve the overall return, while capping the capital risk to a very minimal of the overall portfolio.

The companies we have invested in, have inherent anti-fragile businesses – their solutions are always in demand – whether the economy is expanding or contracting. The Enterprise SaaS solutions we invest in have a significant impact on the business operations of their customers.

The market correction presented a unique opportunity to invest in antifragile businesses that were available at attractive valuation and had built business moats that delivered significant value to customers even in economic slowdowns.

A few examples of antifragility in our portfolio companies:

Credit Nirvana – a debt management and automated collections platform – sees a strong rising demand from customers incase of an economic slowdown / crisis, when the risk of default increases and a strong volume growth in existing customers when the economy is growing, and credit disbursal is pervasive every form of transaction. Credit Nirvana charges its customers a % of the loan book that is managed on the platform. As the customers’ loan book grows, so does Credit Nirvana’s share of revenue from the customer

Blubirch – a reverse supply chain management platform. In a booming economy, its customers see explosive growth in sales – leading to equivalent growth in volume of reverse logistics requiring an efficient technology platform to manage at scale. In an economic slowdown, the customers need to optimize the cost on reverse supply chain, reduce obsolete / damaged inventory and improve working capital – again requiring a technology enabled solution. Blubirch typically charges the customers a % fee of the value of the product shipped, thus scaling with the growth of its customers.

We excitedly look forward to 2023 as we double-down on our investment strategy, identify new areas of investment and look to build an outperforming portfolio of antifragile Enterprise SaaS businesses !

~ Vatsal

Learn more about: CSVP Fund | CGES Index | Enterprise SaaS

Contact Us

contact@csvpfund.comGet our latest updates on

.svg)

.svg)

Contact Us

contact@csvpfund.comGet our latest updates on

Contact Us

contact@csvpfund.comGet latest update here

Contact Us

contact@csvpfund.comGet latest update here

Copyright © 2025 Cornerstone. All Rights Reserved.